How to calculate cash flow?

Free Cash Flow = Net income + Depreciation/Amortization – Change in Working Capital – Capital Expenditure. Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in Working Capital. Cash Flow Forecast = Beginning Cash + Projected Inflows – Projected Outflows = Ending Cash.

Free Cash Flow = Net income + Depreciation/Amortization – Change in Working Capital – Capital Expenditure. Operating Cash Flow = Operating Income + Depreciation – Taxes + Change in Working Capital. Cash Flow Forecast = Beginning Cash + Projected Inflows – Projected Outflows = Ending Cash.

FCFE is calculated as Net Income + Depreciation and Amortization (D&A) – Change in Net Working Capital – Capital Expenditures (Capex) + Net Borrowing.

The simplest way to calculate free cash flow is by finding capital expenditures on the cash flow statement and subtracting it from the operating cash flow found in the cash flow statement.

Net-cash flow - net cash flow is the difference between all cash inflows and all cash outflows of a business: net cash flow = cash inflows – cash outflows.

A cash flow statement tracks the inflow and outflow of cash, providing insights into a company's financial health and operational efficiency. The CFS measures how well a company manages its cash position, meaning how well the company generates cash to pay its debt obligations and fund its operating expenses.

What is a cash flow example? Examples of cash flow include: receiving payments from customers for goods or services, paying employees' wages, investing in new equipment or property, taking out a loan, and receiving dividends from investments.

- Operations: Net income plus any non-cash expenses such as depreciation and amortisation.

- Working Capital: Change in accounts receivable, accounts payable, and inventory.

- Fixed Assets: Total change in fixed assets before depreciation.

Cash Flow to Creditors and Stockholders

Their calculation is similar to that of cash flow from assets. Cash flow to creditors is interest paid less net new borrowing; cash flow to stockholders is dividends paid less net new equity raised.

Free cash flow = sales revenue – (operating costs + taxes) – investments needed in operating capital. Free cash flow = total operating profit with taxes – total investment in operating capital.

What is free cash flow for dummies?

You figure free cash flow by subtracting money spent for capital expenditures, which is money to purchase or improve assets, and money paid out in dividends from net cash provided by operating activities.

Cash profit is a measure of a company's financial health, calculated as the cash inflows from operating activities minus the cash outflows from operating activities.

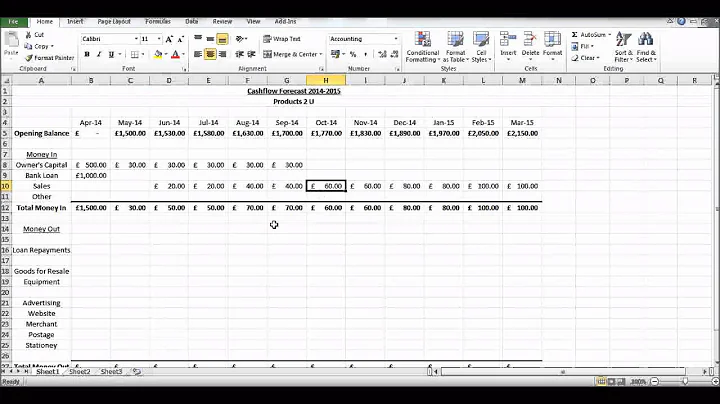

The beginning cash balance is the ending cash balance from the previous period giving a starting point to work from when adding up all of the new cash inflows and outflows during the current period.

- Cash flow from operations = Funds from operations + changes in working capital.

- Funds in operations = Net income + depreciation + amortisation + deferred taxes + investment tax credit + other funds.

There are three cash flow types that companies should track and analyze to determine the liquidity and solvency of the business: cash flow from operating activities, cash flow from investing activities and cash flow from financing activities. All three are included on a company's cash flow statement.

A cash flow statement tells you how much cash is entering and leaving your business in a given period. Along with balance sheets and income statements, it's one of the three most important financial statements for managing your small business accounting and making sure you have enough cash to keep operating.

So, is cash flow the same as profit? No, there are stark differences between the two metrics. Cash flow is the money that flows in and out of your business throughout a given period, while profit is whatever remains from your revenue after costs are deducted.

A “good” free cash flow conversion rate would typically be consistently around or above 100%, as it indicates efficient working capital management. If the FCF conversion rate of a company is in excess of 100%, that implies operational efficiency.

Cash flow refers to money that goes in and out. Companies with a positive cash flow have more money coming in, while a negative cash flow indicates higher spending. Net cash flow equals the total cash inflows minus the total cash outflows.

Let's say a company called Red Bikes has just opened and earned a net income of $75,000 to start and generated additional cash inflows of $95,000. Cash outflows (expenses like rent and payroll) totaled $25,925. This leaves an ending cash balance of $144,075.

Can you calculate cash flow from balance sheet?

Cash flow for non-cash items is calculated by adjusting the company's net income based on differences in revenue, expenses, and credit over a time period. The differences used to make the adjustments are taken from two or more balance sheets and income statements.

Enter "Total Cash Flow From Operating Activities" into cell A3, "Capital Expenditures" into cell A4, and "Free Cash Flow" into cell A5. Then, enter "=80670000000" into cell B3 and "=7310000000" into cell B4. To calculate FCF, enter the formula "=B3-B4" into cell B5.

Use your cash flow statement to determine your total business expenses for a given year. Divide your total expenses by 12 to arrive at an estimate of your typical expenses per month. Multiply that number by the number of months you determined above. That will be the ideal amount to keep in your cash reserves.

The usual guideline is that your business should have 3 to 6 months' worth of operating costs in cash at any one moment. The idea is that you will have enough funds even if there are a few months when you have no cash inflow.

Free Cash Flow to Equity (FCFE) = Net Income - (Capital Expenditures - Depreciation) - (Change in Non-cash Working Capital) + (New Debt Issued - Debt Repayments) This is the cash flow available to be paid out as dividends or stock buybacks.